Golden Energy Resources – Acquisition spread turned into special situation

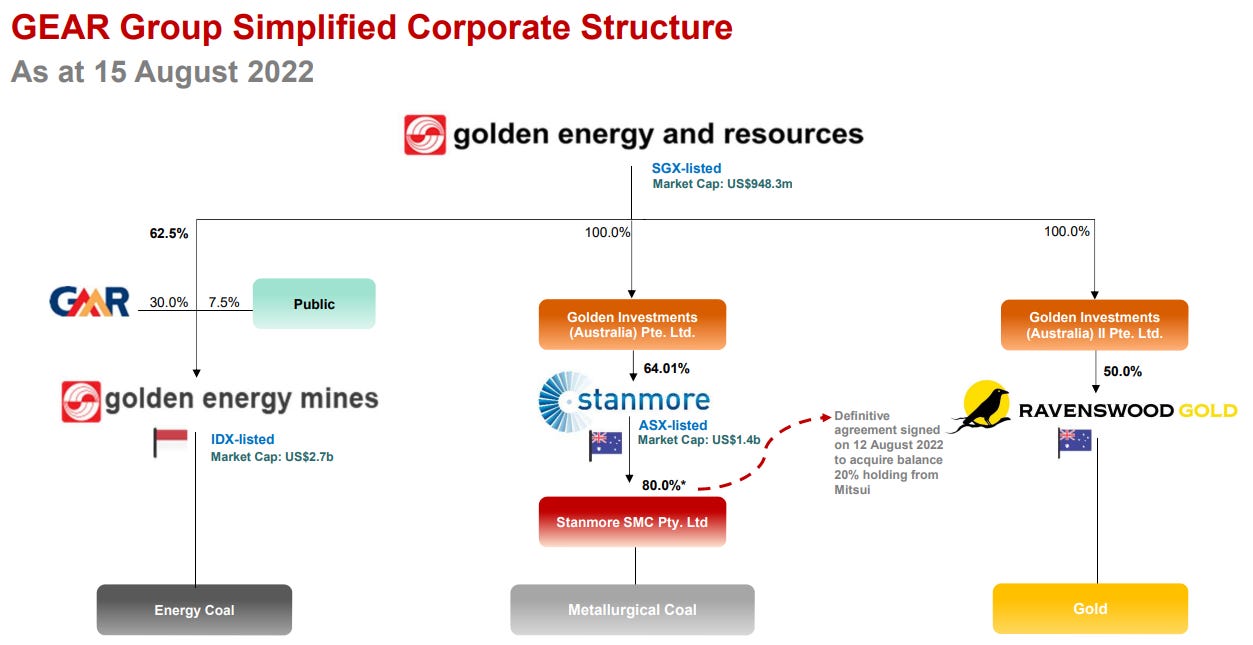

Golden Energy Resources is a Singapore traded company with interests in Golden Energy Mines and Stanmore Resources.

Disclaimer: This content does not consitute investment advice. Investing in cyclical companies requires deep knowledge of the stock and the market they’re based off. You are responsible for your own investment decisions, so do your own research. I hold long positions in the stock mentioned here today.

Today’s article is about Golden Energy Resources (GEAR from now on), a Singapore-based company trading under the ticker AUE, with a 62.05% interest in Golden Energy Mines (GEMS), an indonesian coal company trading under the ticker GEMS in the Jakarta Stock Exchange and a 64.01% stake in the Australian-traded met coal company Stanmore Resoures (ASX: SMR). They also own a 50% stake in an australian gold mine.

A quick summary

GEAR’s major shareholder (the Widjaja family), which owns around 78% of the shares outstanding, made an offer to acquire the entire company back in November 9th 2022. The circumstances of the offer were quite shady as I documented here while it was happening.

In essence, Golden Energy Resources dropped by a 27.22% in a single day, from 0.9 SG$ to 0.655 SG$, with no information at all that could warrant such drop and right the next day they announced the acquisition offer at 0.846 SG$, a price lower than the opening price of the previous day.

Pure coincidence, right?

The current spread of the acquisition is around 2 to 6% and it should close before August 2023. But I also believe there is a good chance that the offer will be raised and I see the downside scenarios as unlikely given that the acquisition is extremely profitable for the Widjaja family.

The acquisition offer

The acquisition offer consists of the following:

Let’s separate the two different parts of the acquisition offer:

They’re offering 1.3936 GEMS shares for every GEAR share or opt for a cash option of 7664.8 Indonesian Rupiah per GEAR share.

Something to note is that since the offer was made the exchange rate of the Indonesian Rupiah to Singapore Dollar has weakened so if shareholders opt for the cash option they will receive ~0.8345 SG$ instead of 0.846 SG$.

For the second part, they are paying 0.16 SG$ for the holding company ex-GEMS shares, which consists of the following:

· Golden Energy’s 50% stake in a JV gold mining business called Ravenswood Gold. They acquired it in 2020 for around 50M AUD (100M on a 100% basis). Ever since then they’ve been pouring around 50M$ in CAPEX for every semester. GEAR has invested a total of around 230M$ in the JV. Yet, the mine is still unprofitable so it’s a bit hard to really value it, but for a conservative valuation, I’ll just discount a 50% of the entire investment over the past three years, so I value their stake in the Ravenswood JV at 115M$.

· Golden Energy’s associated net debt which I calculate it to be around 115M US$ right now. The net debt figure has improved substantially since their latest 1H 22’ results because of the dividends from GEMS.

· Golden Energy’s 64.01% stake in Stanmore Resources, worth 1400M US$ at 3.53 AUD/sh.

The crown of the jewel of the acquisition for the Widjaja family really is the Stanmore Resources’ stake.

Economics of the acquisition: GEMS

According to the acquisition statement the rationale behind the offer is to exit the thermal coal business of GEMS and focus on Stanmore’s metallurgical coal segment. They clearly prefer SMR’s business, since GEAR already made an offer to acquire the company around 3 years ago.

But at the same time, the thermal business is still very attractive given Indonesian Coal prices and in my opinion they are banking on the fact that it’s likely that a lot of shareholders will opt for the cash option of the offer instead of taking GEMS shares. The company trades in Indonesia and it's not easy to get a local broker as a foreigner non-resident.

Either way, I think it’s quite fair they’re paying a ~25% discount to the traded share price, since the liquidity on those shares is low, so even if you decide to take the shares you might not be able to sell them at current market prices.

Economics of the acquisition: Exit Offer & SOTP

Before getting into the numbers let me say I find this part of the offer very unfair, the Widjaja family stands to make hundreds of millions of dollars from a simple financial transaction.

Given that they intend to pay 0.16 SG$ for this part and that there are 2638.1M shares outstanding it would be total cost of 422M SG$ or 321.2M US$. Since the Widjaja family already owns 77.5% of the shares outstanding the total acquisition cost will only be a 22.5% of that (95M SG$ or ~72.4M US$).

To calculate how much the stake could be worth I’ve done a sum of the parts valuation.

Ravenswood gold: A 50% discount to their total investment over the past three years - 115M$.

Stanmore Stake: 64.01% stake at traded market value.

Net debt: Given that GEAR has received around ~165M$ in dividends from GEMS on the second half of 2022 I estime the net debt to be around 115M$.

So the net value of the company would be around 317M$. To give an easier comparison this would equate to 0.71 SGD per share and their intention is to pay only 0.16 SGD for it.

I want to insist that most of the value of the offer resides in Stanmore Resources, a liquid traded security. We can argue about the Ravenswood Gold value, but even if you write it off and consider its value as 0 the SOTP valuation would still be 0.646 SGD per share for an immediate 400% upside to the acquiror.

I also want to insist in the sheer amount of money they stand to make from a simple financial transaction: over 300M$. There is no execution risk: no mine or oil field to be developed, this is simply buying a traded asset way below its traded value.

Will the offer be raised?

The Widjaja family stands to make an obscene amount of money even if they raise the offer substantially. I also want to point out that this transaction should be closed by August, but in the meantime there is the possibility that GEAR will receive additional dividends from GEMS, making the offer even more attractive.

But, why would they raise the offer if they don’t need to? There are two scenarios in which they could be forced to do it.

They could simply lose the vote to shareholders. They need a 75% of the independent votes in favour for the offer to go through. The reality is that so far there is not a big shareholder or an activist, so even though the offer is very unfair they could still get the votes. They are also threatening, in a way, that if the offer goes through and you vote against it, you’re going to be stuck with the shares in the private company.

Being forced to raise it by the Singapore Stock Exchange. Before the offer goes through there needs to be an independent financial advisor reviewing the deal. Even if this “independent” advisor is not very independent (we know these things happen) I just don’t see how they are going to justify paying such a big discount to tradeable securities.

I honestly don’t know if the Singapore Stock Exchange is usually aggresive in these kind of takeovers, but in the time I’ve been investing I’ve found the SGX to be a lot more dedicated to the protection of shareholders than in other exchanges. The SGX usually asks open questions related to the financial results or trading activity of their companies. This is the questions they sent regarding GEAR’s weird trading activity the day before the offer.

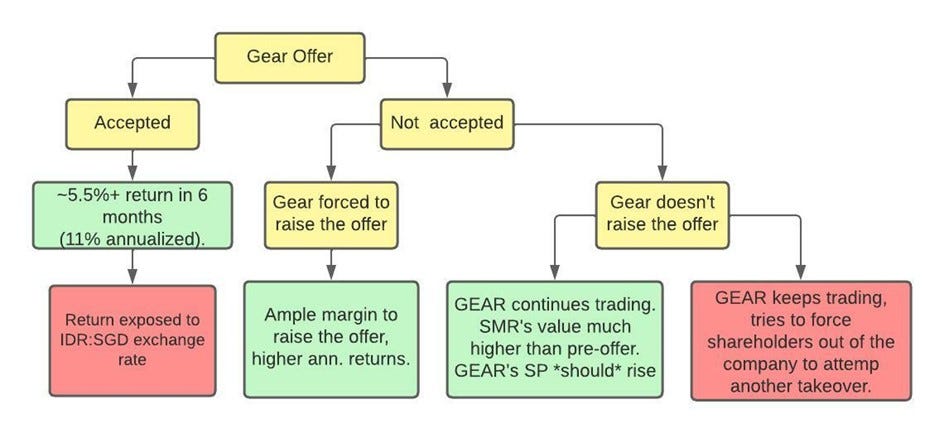

Possible outcomes

These are the possible outcomes of the transaction:

When it comes to the spread it is a lot thinner now than just last week when I was writing the article. GEAR went up by 0.025 SGD today (6th Feb) so at 0.82 SGD the spread is around 1.7% which is obviously not very attractive.

Case 1: The acquisition offer is accepted.

You make the spread based on your purchase price and the price they’re paying. At 0.79 SGD that is over 5.5% or 11% annualized.

Case 2: They raise the offer:

They have an ample margin to raise the offer and still have an extremely profitable deal. We’re talking that at current prices they are making over 300M$ with little execution risk. Even if they doubled the offer to 0.32 SGD they would still make over 140M$. At 0.64 SGD, or four times the current offer, they would simply be paying the sum of the parts even if we consider Ravenswood value as 0.

You could even argue that they should pay a premium to the value of traded securities, but I will be happy if they double the offer. If they double the offer the current spread would be around a 25%, or almost 50% annualized.

Case 3: The offer is not accepted and they don’t raise the offer.

In this scenario we would own the company which at the current price of Stanmore Resources it looks like a pretty good deal.

For instance, at 0.79 SG$ the company’s market cap is 1.58B US$, they have around 115M$ in net debt and their stake in Stanmore is already worth 1.5B$. Apart from that they own a 60%+ of the indonesian miner which is still extremely profitable and has been paying consistent dividends over this past year.

In my opinion the biggest likelyhood would be for the offer to be accepted or for the offer to be raised. As I said they can make hundreds of millions of dollars despite paying more.

Reflection: Is the voting process fair?

Edit 10th of February: I initially thought that shareholders that voted against the offer couldn’t tender the shares, but it seems that shareholders will be able to vote against the offer and still have 14 additional days to tender the shares.

Therefore I intend to vote against the offer and if it still goes through I will tender my shares.

Thanks to Jeremy Raper for the information- https://twitter.com/puppyeh1

thanks for the article but I need to make a very important correction. Even if you vote No, the Exit Offer will be open for a period of 14 days once all Exit Offer conditions have been fulfilled, for ALL shareholders (even those who vote no) to accept the terms. see pages 13-14 here: http://investor.gear.com.sg/newsroom/20221109_021819_AUE_B599T1IV2BCR696W.1.pdf

In other words, the barrier to voting no here is really much lower than you portray. this is quite a crucial point given the amount of value being extracted here. even if you vote No to try to block the deal - as I obviously am, on these heinous terms - you can still take the Exit Offer in the end if it ends up getting voted through.

Conclusion

I find GEAR to be an interesting situation: we can make a decent spread on the current offer but at the same time there is a good chance that the offer will be improved.

Whatever happens this should be finished by August 2023, so we have a fixed time frame and the annualized returns could be very high if they end up raising the offer.

Thank you for reading the article, I hope you liked it and if you did you can help me by retweeting this tweet:

If you have any questions or thoughts on the article leave a comment here or on Twitter.

thanks for the article but I need to make a very important correction. Even if you vote No, the Exit Offer will be open for a period of 14 days once all Exit Offer conditions have been fulfilled, for ALL shareholders (even those who vote no) to accept the terms. see pages 13-14 here: http://investor.gear.com.sg/newsroom/20221109_021819_AUE_B599T1IV2BCR696W.1.pdf

In other words, the barrier to voting no here is really much lower than you portray. this is quite a crucial point given the amount of value being extracted here. even if you vote No to try to block the deal - as I obviously am, on these heinous terms - you can still take the Exit Offer in the end if it ends up getting voted through.

How do you hedge against the possibility of IDR weakening further against SGD in the interim